China's ascent in antibody-drug conjugates has become difficult to ignore: in just the past year, a once primarily domestic oncology story has turned into one of the most closely watched shifts in global drug development. In the last 12 months alone, some of the biggest highlights include:

-

Record-setting licensing activity: China biopharma out-licensing reportedly reached $137.7 billion in 2025, with ADCs among the most visible areas of global pharma interest.[1]

-

Mega-partnerships with global pharma: Innovent's cancer therapy collaboration with Takeda was valued at up to $11.4 billion, including $1.2 billion upfront, while Hengrui signed large multi-asset global collaborations with GSK and BMS that reinforced China's position as an oncology innovation source.[2][3]

-

Faster clinical and regulatory progress: DualityBio/BioNTech's HER2 ADC program advanced through a China Phase 3 study across 48 sites and 228 patients, while multiple China-linked ADCs moved through approval or late-stage development in breast cancer and other solid tumors.[4][5]

The story is no longer simply that China has a large oncology market. China is becoming one of the world's most important ADC origination markets, with global pharma increasingly looking to Chinese companies for differentiated assets, fast-moving clinical programs, and platforms that can compete globally.

For SaaS or software companies looking to sell into this market, the opportunity is not simply "ADC companies need software." ADC development creates unusually complex workflows around translational evidence, target selection, linker-payload decisions, biomarker strategy, CMC data, toxicology signals, clinical trial design, competitive intelligence, regulatory packages, and global partnering materials. In China, those workflows are often distributed across biotechs, hospitals, CROs, CDMOs, academic labs, and commercial partners, which makes coordination even harder.

That is where the opportunity sits. Software companies that can help Chinese ADC players move faster, reduce development risk, organize evidence, support cross-border collaboration, or make global BD and regulatory work more credible may find a receptive market. Success, however, depends on understanding how China's ADC ecosystem actually works, who controls each part of the workflow, and whether the product solves a practical bottleneck for local teams rather than simply importing a Western sales story.

The signal is unmistakable. What it doesn't tell you is who to sell to.

ADC development in China takes on a more distributed workload compared to Western markets, where many of these functions can sit inside a single sponsor organization. In China, a biotech sponsor defines the strategy and owns the asset, but execution flows simultaneously across CROs, CDMOs, analytical providers, and platform companies. WuXi XDC, to take one example, has explored more than 5,600 molecules, serves over 640 customers, and runs more than 200 integrated ADC projects, including work with the majority of the world's top pharmaceutical companies. BGI Group has built parallel infrastructure in genomics and data generation. These are not peripheral vendors — they are structural to how programs execute, which means a single ADC program generates data across multiple independent organizations that each operate on their own terms.

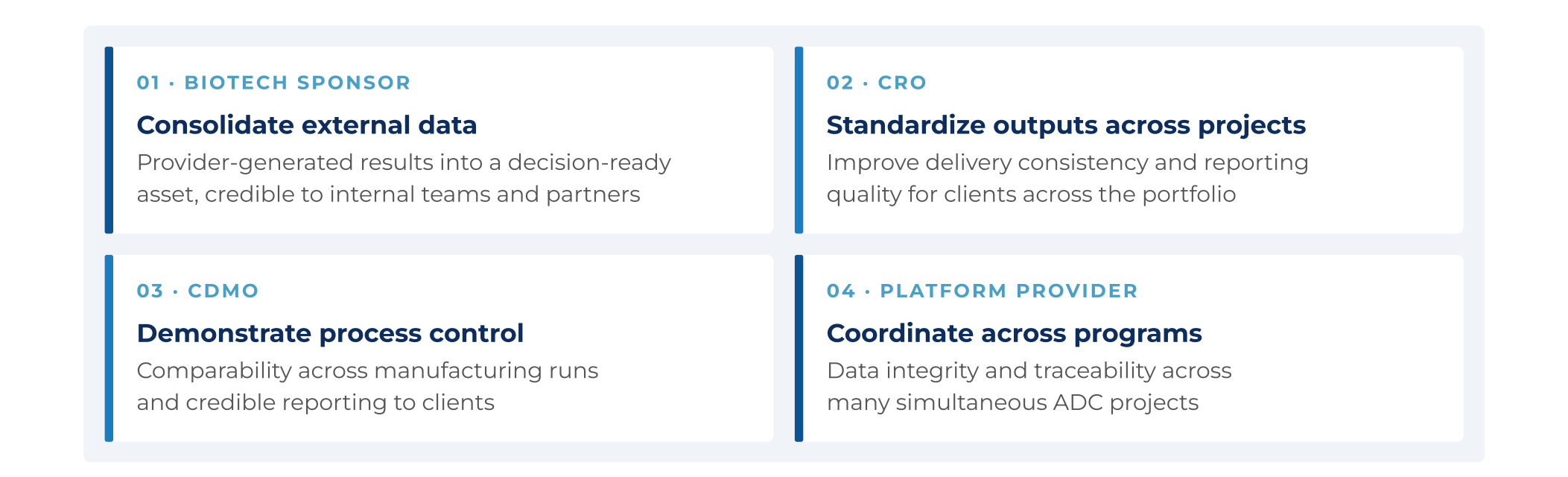

That distribution creates a market structure and opportunity where each company holds real budget and evaluates software against a different outcome. Sponsors need to consolidate data generated by external providers into something they can trust internally and present credibly to partners. CROs need to standardize outputs and improve delivery consistency. CDMOs need to demonstrate process control and comparability across manufacturing runs. Platform providers need to coordinate data across many simultaneous programs while maintaining traceability. A single ADC program does not map to one buyer. The software opportunity is distributed across the same ecosystem that executes the programs.

What This Means for Market Entry

Three best practices for companies targeting China:

Target definition. A product that helps biotech teams consolidate provider-generated data into a decision-ready asset finds its buyer in a head of R&D or translational lead. A product that improves throughput and standardization is a CRO play. One that strengthens process consistency belongs in a CDMO conversation. The market intelligence required to find and qualify these buyers is different for each participant type, which means a single messaging approach misses most of the market.

Ensure data travels. Data rarely stays within one organization. CRO-generated data must be interpretable by the sponsor; sponsor-structured data must be credible to an external partner. Products that support these handoffs become embedded in how programs are tracked and evaluated. Products that function only within a single context limit their own adoption.

Reposition around distributed value. Messaging built around performance within a single workflow misses how buyers in this ecosystem evaluate tools. What resonates is how a product maintains consistency across providers, enables meaningful comparison, and supports decision-making across organizational boundaries.

China's ADC market is one of the most active buying environments in global oncology. The structural difference from Western markets is that demand is distributed across the ecosystem, not concentrated in one buyer type. The vendors positioned to capture it are the ones who have identified their specific participant, aligned their positioning to that role, and built products whose outputs remain useful at the next step in the chain.

Footnotes

[1] Reuters reported that China biopharma out-licensing reached a record $137.7 billion in 2025, and identified patent cliffs and R&D cost-cutting as drivers of global pharma interest in Chinese-developed drugs. https://www.reuters.com/sustainability/climate-energy/china-biotech-licensing-boom-hit-record-2026-pipeline-swells-2026-02-13/

[2] Takeda's announcement states that Innovent would receive $1.2 billion upfront, including a $100 million equity investment. Reuters reported the total deal value as $11.4 billion and described the collaboration as covering immuno-oncology and antibody-drug conjugates.

[3] BMS stated that its Hengrui agreement could reach approximately $15.2 billion in total potential value, including upfront and milestone-related payments across oncology, hematology, and immunology programs.

[4] BioNTech and DualityBio reported that the Chinese randomized Phase 3 trial of trastuzumab pamirtecan / DB-1303 / BNT323 enrolled 228 patients across 48 trial sites and compared the ADC against T-DM1.

[5] Daiichi Sankyo reported Datroway's China approval for metastatic HR-positive, HER2-negative breast cancer and described it as the second DXd ADC approved in China after Enhertu. Kelun-Biotech reported NMPA approval of trastuzumab botidotin for HER2-positive breast cancer and described it as China's first domestically developed HER2 ADC broadly covering 2L+ HER2-positive breast cancer patients.

Additional Sources

-

AstraZeneca, Full Year and Q4 2025 Results Announcement https://www.astrazeneca.com/content/dam/az/PDF/2025/Q4-FY/Full-year-Q4-2025-results-announcement.pdf

-

BCG, "Emerging New Drug Modalities in 2025 https://www.bcg.com/publications/2025/emerging-new-drug-modalities

-

WuXi XDC, "WuXi XDC Delivers Exceptional Performance in 2025" https://wuxixdc.com/wuxi-xdc-delivers-exceptional-performance-in-2025-reinforcing-global-leadership-in-bioconjugate-crdmo/